Aura Energy, The Australian Company Behind New Sweden

Aura Energy Limited is an Australian-based mineral company specialising in the exploration development of uranium and polymetallic projects across Africa and Europe, which I stumbled upon while reading an article on Sweden’s vote to allow uranium mining (WNN, 2025). My perspective as an investor naturally led me to want to know who would be involved in this process. Aura Energy (ASX: AEE, or AIM: AURA), a promising yet mispriced stock relative to its asset quality and project economics, is trading at a valuation consistent with high-risk exploration juniors, while possessing:

A fully permitted near-term uranium mine (Tiris, Mauritania) with high-margin economics (NPV₈ US$499m, IRR 39%, payback 2.25 yrs).

A 49% increase in proved + probable reserves to 33.6 Mlbs U₃O₈, materially de-risking the production profile.

An enormous 800+ Mlbs U₃O₈ control over 100% of Häggån’s resource in Sweden, historically stranded by regulation but now unlocked by the Swedish government’s decision to lift the uranium mining ban in 2026,

Commercial milestones (offtake agreements covering ~25% of 2028–2031 production and long-term US utility) that reduce price risk and create financing credibility.

A strong catalyst path: financing (DFC), FID (2026), construction (2026), and production (2027).

AEE is being valued as a mere speculative explorer despite already having permitted assets, reserves, contracts, and a credible funding process.

·“Swedish parliament votes to allow uranium mining.” World Nuclear News, 2025, www.world-nuclear-news.org/articles/swedish-parliament-votes-to-allow-uranium-mining.

Industry Context (Why Now)

Demand Conditions

Global uranium demand is projected to increase by 28% toward 2030 due to nuclear expansion (WNA).

Australia's uranium sector is already riding a wave of demand as tech giants like Google, Amazon, and Microsoft lock in nuclear power to fuel their AI data centres.

Nuclear energy is becoming the preferred solution due to its clean and continuous nature.

One can speculate that Australia’s supply will be insufficient for tech giants in the long term.

Supply Conditions

One can speculate Australia’s supply will be insufficient for tech giants long-term.

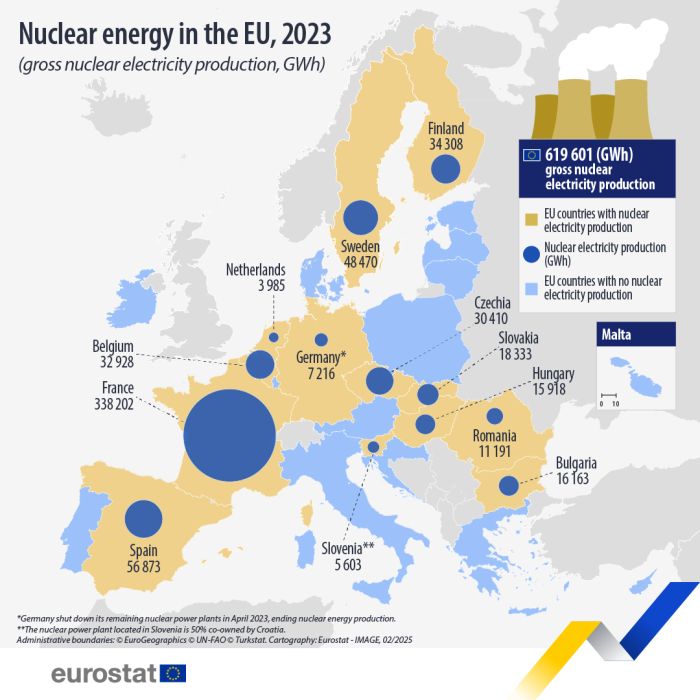

Sweden holds ~27% of EU uranium. Haggan’s scale (>800Mlbs) makes Aura one of the key strategically important Western-listed uranium owners once the ban is lifted on the 1st of January 2026.

Project 1: Tiris Uranium Project (Mauritania)

What is Tiris?

Tiris is Aura's flagship asset: a fully permitted, near-term uranium mine located in Mauritania, Africa. Why Does Tiris Matter?

Why Does Tiris Matter?

Tiris transforms AEE from an "explorer" into a de-risked developer and soon-to-be producer. The project's quality gives AEE inherent value, independent of market speculation.

Robust Economics: The project is projected to generate massive returns with a net present value (NPV) of US$499 million and a rapid payback period of 2.25 years.

Contracts: De-Risk Funding: AEE has already secured long-term contracts covering approximately 25% of its 2028–2031 production. This commercial progress provides price protection and is critical for securing the necessary US$230M development capital from organisations like the DFC (Development Finance Corporation).

Near-Term Cash Flow: With construction planned for 2026 and first production in 2027, Tiris will provide the crucial cash flow to support the company’s valuation and future growth.

Project 2: Haggan (Sweden)

What is Haggan?

In my thesis, Haggan stands out as a significant resource. It is one of the world's largest fully undeveloped uranium and multi-commodity resources. It is located in Sweden, a stable, Western-aligned jurisdiction. A government ban on uranium mining has "stranded" the project for nearly a decade.

Why Does Haggan Matter?

Haggan is the asymmetric upside, the "free option"that currently holds minimal value in the market but has the guaranteed potential for a substantial re-rating:

The Regulatory Unlock: The Swedish government will lift the uranium mining ban on January 1, 2026. This single legislative act immediately unlocks Haggan's value.

Massive Scale: The resource holds over 800 million pounds of triuranium octoxide. To put this in perspective, this scale is equivalent to that of existing mid-tier uranium producers.

Material Valuation Impact: Even without uranium, the 2023 Scoping Study for the other commodities (like vanadium and nickel) showed an NPV range of US$380M–US$1.23B. Including the uranium resource would materially increase the NPV and is the key driver of long-term value.

Financial Position & Security Analysis

Asset Strength and Backing

The true value of AEE lies in its capitalised assets, not its current cash flow:

Growing Asset Base: The value of the Uranium Segment Assets increased significantly from A$30.26 million (30 Jun 2024) to A$38.92 million (30 Jun 2025). This rapid growth reflects management's successful investment into and de-risking of the Tiris project, providing tangible book value support for the projected US$499M NPV. The overall capitalised exploration & evaluation asset jumped to A$50.5M (30 Jun 2025), underpinning the Tiris and Haggan projects.

Haggan's Book Value: The Vanadium Segment Assets are recorded at A$12.21 million (30 Jun 2025). This is the concrete financial evidence of the Haggan project's multi-commodity potential, reinforcing that the optionality is a tangible, valued asset on the balance sheet, not just a theoretical resource.

Eurostat, 2023, Nuclear Energy Gross Enery Production in EU (GWh).

Debt Profile and Liquidity

The company maintains a strong financial structure heading into its critical funding phase:

Clean Debt Structure: The company carries minimal liabilities on its core segments and reported virtually no long-term debt on the consolidated balance sheet. This clean structure is a significant advantage when seeking low-cost debt financing from institutions like the DFC, as the Tiris asset can be easily secured.

Liquidity: The cash and cash equivalents stood at A$11.7M as of 30 June 2025. This cash position supports a short-term runway but highlights the urgent need to secure project financing, which is the primary source of investor risk.

Understanding the Loss: The Net Loss of A$15.34 million (30 Jun 2025) is largely driven by non-cash share-based payments (A$6.28 million) and corporate administrative expenses (A$5.04 million).

Capital Structure & The Funding Gap

The primary risk and source of the market's mispricing is the funding gap:

Funding: The required Tiris Project CAPEX is US$230M, which contrasts sharply with the current A$11.7M cash balance. This delta drives the financing risk argument.

Dilution Pressure: The need to bridge this funding gap, combined with the presence of loan-funded shares issued to directors and recent placements (9 million A$ in December 2024), creates a form of dilution risk.

Mitigation: The active pursuit of DFC financing and strategic partner investments is designed to secure high-quality, lower-cost capital, which minimises reliance on equity placements and directly counters the dilution risk argument.

The Sum-of-Parts (SOTP) Framework

1. Tiris (Near-Term Operation): Base Value

The Tiris project, fully permitted and highly de-risked, provides the base intrinsic value for AEE.

Discounting for Risk: Given that the project still requires US$230M in CAPEX and faces execution risks, we apply a probability-weighted discount. However, considering the strong IRR of 39% and the advanced DFC process, a 30% discount is reasonable to account for financing and execution.

Weighted Value Estimate: US$349M (or A$529M).

2. Haggan (Long-Term Optionality): The Asymmetric Upside

Häggån is currently priced as a zero-value option, yet its scale and the imminent regulatory change are transformative.

Resource and Non-Uranium Value: The project controls >800 Mlbs, and the non-uranium components alone show an NPV range of US$380M–US$1.23B.

Optionality Weighting: I assign a low-probability but meaningful 5% weight to the midpoint NPV of US$805M. This valuation is conservative, acknowledging the timeline and the need for new uranium-inclusive studies.

Weighted Value Estimate: US$805M times 5% = US$40M (A$61M). This addition is pure accretion for investors buying at today's price.

3. EV/lb Benchmark

Enterprise Value per pound (EV/lb) is a metric used in the uranium mining industry to compare the cost of a company's uranium resources per pound of uranium.

AEE's current Enterprise Value (EV) per pound of reserve is significantly lower than that of its peer developers. Once the Tiris FID is announced and the Haggan unlock occurs, the market will be forced to re-rate AEE to align it with producing peers, effectively closing the valuation gap and delivering substantial returns.

Risks

The primary risk and source of the market's mispricing is the funding gap, as mentioned before.

In addition:

· Regulatory Risk: A delay in the Swedish legislation timeline (expected January 2026) would delay the Haggan re-rate.

· GeologicalRisk: of Tiris's LOM production is based on inferred resources (resources based on limited sampling and based on reasonably assumed but limited information).

Catalysts

The company has a dense schedule of high-impact catalysts over the next two years that will force a market re-rating:

Funding package completion (DFC/strategic equity)

Swedish ban lifted (Jan 2026)

Final Investment Decision (FID) for Tiris (early 2026)

Construction starts (2026)

First production (2027)

Additional exploration results at Mauritanian tenements

Conclusion

Aura Energy presents a rare case where the market valuation remains anchored to an outdated perception of a speculative African explorer. The company possesses full permits, high-quality economics, large reserves, and strong geopolitical alignment and has a big piece of the pie in the transformative policy change in Sweden.

The SOTP framework confirms a substantial disconnect between the intrinsic project value (anchored by the US$349M weighted Tiris NPV and the current market cap). The stock trades today as if Häggån is worthless and Tiris is unlikely to be built. I believe the impending DFC funding, coupled with the Häggån legislative unlock, will resolve the market's mispricing. The result is an attractive opportunity for value-orientated investors.